Rural Bank, Media Release, 4 July 2023

Rural Bank’s Australian Agriculture Mid-Year Outlook 2023 report finds that favourable seasonal conditions and strong production over the first half of 2023 ensured strong winter crop establishment and pasture growth, particularly on the east coast, but despite a positive start to the year, softening commodity prices are now impacting Australian farmers following several seasons of strong prices.

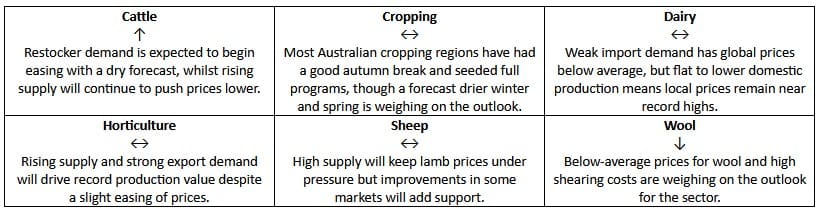

The report analyses the performance of six industries – cattle, cropping, dairy, horticulture, sheep and wool, with producers generally well positioned following a good start to 2023 – however, other factors such as a slowing global economy combined with drier seasonal conditions are now in play and weighing on the outlook for 2H 2023.

Andrew Smith, Rural Bank Head of Agribusiness Development said: “Three key themes to impact Australian agriculture in the second half of 2023 are dry seasonal conditions, trade conditions and the persistent economic headwinds now swirling across the globe, from which we are not immune.”

“A higher Australian dollar is also expected to weigh on the competitiveness of Australian agricultural exports, but overall, we expect marginal impact with our dollar still sitting below historic averages. Below median rainfall is very likely across most of Australia over the next six months and it’s this drier seasonal outlook that’s now weighing on production forecasts across a range of agricultural commodities.

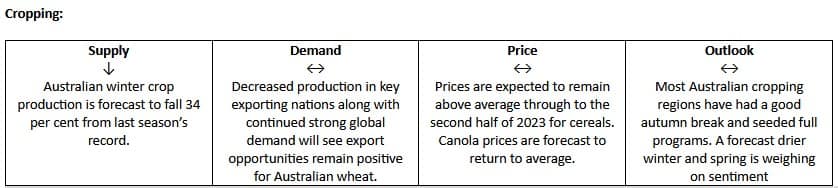

“Australian winter crop production is also expected to fall from the record output recorded last season with national winter crop production now forecast to come in slightly below average – though a strong autumn break and timely rainfall in early June is supporting a strong start to the season.

“The Russian invasion of Ukraine continues to drive volatility across both grain and oilseed markets as ongoing uncertainty surrounding exports from two of the largest grain producing nations continues, however, the ongoing diversification of our export markets will hold Australian exporters in good stead, despite the ongoing volatility in grain markets.

“While we forecast horticultural production to remain strong despite the drier outlook, consecutive seasons of herd and flock rebuilding across livestock industries are also expected to drive stronger beef and lamb supply into the back half of the year.

“In terms of input costs, the recent welcome rebound observed in both net migration and working visa approvals is helping to alleviate labour shortages, particularly across the agricultural sector, with a general easing of fertiliser prices and pandemic induced supply chain issues also welcome, with these reduced input costs supporting grower margins amidst the broader decline in commodity prices seen across the first half of 2023”.

“A positive for Australian farmers is that both global bulk and container shipping rates have now returned to pre-pandemic levels as the slowdown in global economic activity softens freight demand and we continue to see trade relations between China and Australia improving”, Mr Smith concluded.

National snapshot

Fast facts

- From the field

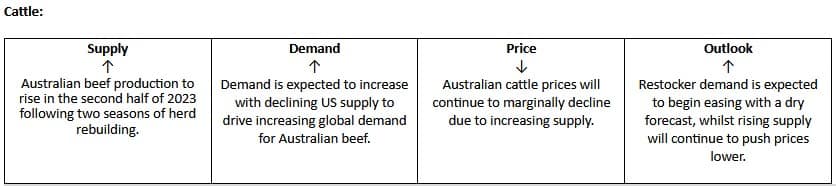

“Australian cattle prices are likely to remain softer in the coming months as supply on the market remains constant given the tough season being experienced in some cattle areas. Seasonal conditions will be the key influence on supply as producers weigh up whether to hold onto cattle or sell given the current drier outlook for the remainder of the year”.

Mark Pain, Senior Agribusiness Relationship Manager – Queensland.

- From the field

“Widespread rainfall across Victoria in early June has allowed growers to finish off seeding and get mostly full programs in. The rainfall was very timely after a dry May and was the break growers were waiting for, especially in the northern Wimmera and Mallee regions. This has transformed Victoria’s grain production potential from one of below average to at least average. With the likelihood of an El Niño developing by spring remaining high, growers will be cautious in putting on forward sales until September”.

Wayne Saunders, Regional Manager Agribusiness – Western Victoria.

- From the field

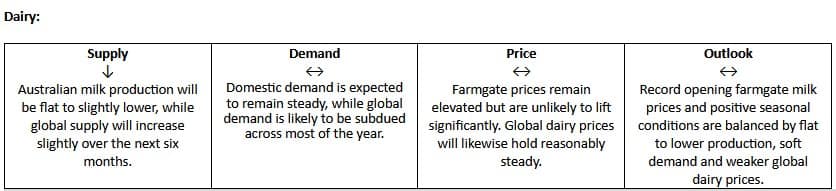

“Strong farmgate milk prices and positive seasonal conditions provide optimism for a profitable season ahead. Good returns will likely see production stabilise after consecutive years of decline in the face of labour shortage and increased input costs. Australian dairy prices appear to be increasingly disconnected from global conditions with contracting local production increasing the threat of imports from other regions”.

Tony Anderson, Regional Manager Agribusiness – South Victoria.

- From the field

“Favourable soil moisture and low irrigation costs will drive strong production volumes, despite the prospect of dry weather conditions over the coming months. Fruit and vegetable prices are broadly expected to ease but remain broadly above average, with supply chains back to normal following last year’s floods. While margins remain thin: strong production forecasts, softening fertiliser prices and improved labour supply is driving increased optimism within the industry following a challenging 12 months”.

Leah Weekes, Regional Manager Agribusiness – Queensland.

- From the field

“Lamb markets are expected to encounter good numbers of new season lambs in the second half of 2023. As high supply continues, markets will be looking for direction from export demand which has been a mixed bag so far this year. A drier outlook should avoid the challenges presented by the wet conditions of late 2022 which culminated in a surge of supply in recent months”.

Stuart Bear, Senior Agribusiness Relationship Manager – Ballarat.

- From the field

“Global economic headwinds are providing downward pressure on the forecast outlook for wool prices. This, coupled with local skilled labour supply shortages and increased costs for wool harvesting will see sentiment in flock re-stocking by Australian wool and sheep farmers in the short-term. Attracting and retaining wool harvesting labour continues to be a focus for the industry and grower groups”.

Matt Gill, Senior Agribusiness Relationship Manager – Central and North-East Victoria.

Across the country: State by state fast facts –

Queensland forecast

- Strong avocado production is again anticipated across the Queensland growing regions as recent plantings continue to mature. A lack of access to the Japanese market for Queensland growers leaves prices more vulnerable to the increased domestic supply seen across the state.

- Current industry forecasts have the 2023 macadamia crop sitting at around 60,000 tonnes in shell, an increase on last year’s crop of almost 53,000 tonnes. Both domestic and export demand remains subdued as inflationary pressures weigh on consumer demand for premium produce which is weighing further on pricing which is near ten-year lows.

- Queensland growers have mostly finished planting the 2023/24 winter crop. Conditions have allowed for full programs to go in which sees planted area largely unchanged from last season. Prices will remain supported due to tight ending stocks from a strong 2022/23 export program along with a dry outlook that will see growers with stock hold onto them until the season outlook becomes more certain.

- Queensland cattle prices are expected to continue to soften throughout Q3 as rising supply on the market push prices lower, however Q4 is likely to see prices rise. Cattle slaughter in Queensland is expected to remain firm, but ongoing labour issues could limit significant growth.

- Wool prices will continue to come under pressure as demand eases amidst weakening economic conditions. The Northern Regional Indicator now sits at 1,195 cents. The price differential between fine and medium merino wool has begun to close as finer wools record larger declines with medium wools already near historic lows. The Eastern Market Indicator (EMI) is expected to remain below 1,350 cents.

- Queensland sheep numbers are building mainly through increases in Merinos which has driven significant production with a 18.9 per cent year-on-year progressive gross weight increase as of June 2023. The gains can also be attributed to heavier fleece weights seen as a result of delays to shearing due to ongoing shearer shortages.

- Queensland milk production is expected to stabilise in the 2023/24 season following five seasons of declining production, but remain below average.

- Opening farmgate milk prices remain near record highs with Norco offering 88c/litre and Lactalis lifting to 89.5c/litre after producers expressed disappointment with opening prices. High farmgate milk prices and the declining value of beef are expected to contribute to a slowdown of industry exits.

New South Wales forecast

- Lamb markets are expected to encounter good numbers of new season lambs in the second half of 2023. As high supply continues, markets will be looking for direction from export demand which has been a mixed bag so far this year. A drier outlook should avoid the challenges presented by the wet conditions of late 2022 which culminated in a surge of supply in recent months.

- While the Bureau of Meteorology’s forecast for below median rainfall across much of the country is a concern, high water storage levels are keeping water prices low which will continue to benefit irrigated crops.

- Potato volumes have returned closer to average over the past quarter, though production remains hampered following a challenging six-month period for producers. Later plantings are struggling with a lack of sunlight due to shorter days, which becomes more of an issue later in the year. This may have a negative impact on yields.

- Cropping conditions remain mixed in New South Wales. Southern regions have seen favourable autumn conditions which has allowed full programs to be planted and good crop establishment. Northern New South Wales remains dry with some growers yet to plant crops. If conditions remain dry in the north through July, we could see planned winter crop area forecasts decline further from current estimates.

- New South Wales dairy production continues to be affected by labour availability, but industry surveys show most businesses are optimistic about profitability for the coming season. Farmgate milk prices averaging around $9.00-$9.15/Kg MS are expected to remain relatively static in coming months.

- While below record highs seen last season, elevated farmgate milk prices are expected to see production flat to slightly lower than last year as industry exits slow down.

- New South Wales cattle prices are likely to see a continued fall in the second half of 2023 as ongoing pressure from increasing supply on the market applies downwards pressure on pricing.

- The price differential between fine and medium merino wool has begun to close as finer wools record larger declines with medium wools already near historic lows with the Eastern Market Indicator (EMI) expected to remain below 1,350 cents. The Northern Regional Indicator now sits at 1,195 cents. 2022/23 Wool production in NSW is now in line with the previous season in terms of progressive gross weight and overall bales sold with volumes rebounding following NSW shearing delays. Many sheep producers have retained older ewes and Merino lambs due to the drop in sheep meat prices which will keep wool supply elevated in the back half of the season.

Victoria forecast

- While the Bureau of Meteorology’s forecast for below median rainfall across much of the country is a concern, high water storage levels are keeping water prices low which will continue to benefit irrigated horticultural crops.

- This year’s almond crop has been impacted by a number of challenges, with initial estimates putting total output for the 2023 crop well below last year’s almond crop of almost 140,000 tonnes. Difficulties with pollination driven by the varroa mite outbreak last year along with a wet finish to 2022 drove a significant decline in yields.

- Orange production volumes are expected to decline slightly with average yields and slightly smaller sizing, though overall quality is looking good.

- Potato volumes have returned closer to average over the past quarter, though production remains hampered following a challenging six-month period for producers. Later plantings across parts of Victoria are struggling with a lack sunlight with shorter days which may have a negative impact on yields.

- Victorian milk production is forecast to lift marginally in the second half of 2023 as the industry recovers from the impacts of flooding, though output will still remain below longer-term average. Labour remains an issue, but positive seasonal conditions and high farmgate prices at around $9.00/Kg MS are expected to stem the flow of industry exits.

- Victorian growers have finished seeding their 2023/24 winter crop programs which have gone in under favourable conditions. Widespread rainfall over June has shored up production outlooks with average yields now achievable despite the dry outlook remaining in place.

- Lamb markets are expected to encounter good numbers of new season lambs in the second half of 2023. As high supply continues, markets will be looking for direction from export demand which has been a mixed bag so far this year.

- A drier outlook should avoid the challenges presented by the wet conditions of late 2022 which culminated in a surge of supply in recent months.

- Victoria’s cattle prices are expected to continue the recent trend which started at the beginning of 2023 and trend lower, as strong supply levels push values down. Cattle slaughter is likely to remain firm throughout the next six months, but growth could be capped by labour issues.

- The price differential between fine and medium merino wool has begun to close as finer wools record larger declines with medium wools already near historic lows with the Eastern Market Indicator (EMI) expected to remain below 1,350 cents. The Southern Regional Indicator now sits at 1,101 cents. A strong seasonal break occurred during autumn which will set up good feed for sheep production coming into spring. Wool production in Victoria is down 1.4 per cent year-on-year in terms of gross weight as shearer shortages across the state continue to impact available volumes.

Tasmania forecast

- Potato volumes have returned closer to average over the past quarter, though production remains hampered following a challenging six-month period for producers. Later plantings across parts of Tasmania are struggling with a lack of sunlight due to shorter days, which may have a negative impact on yields.

- Tasmania saw onion plantings impacted by heavy rainfall and flooding which has weighed on output over the first half of 2023. Onion supply is expected to return closer to average over the back half of 2023. Strong export demand from Europe is expected.

- Tasmanian milk production will remain below average for the remainder of 2023 but is anticipated to lift above last season’s lows after recovering from flood-impacted supply chains. 2023/24 production is forecast to be steady as positive seasonal conditions and record opening farmgate prices see producers take advantage of a favourable start to the season.

- Lamb markets are expected to encounter good numbers of new season lambs in the second half of 2023. As high supply continues, markets will be looking for direction from export demand which has been a mixed bag so far this year. A drier outlook should avoid the challenges presented by the wet conditions of late 2022 which culminated in a surge of supply in recent months.

- Tasmania’s cattle prices are likely to continue softening during the second half of 2023 due to downward pressure from increasing supply availability on the market. Slaughter rates and cattle yarding’s are also expected to rise as the industry completes its transition from herd rebuild to growth phase.

- The price differential between fine and medium merino wool has begun to close as finer wools record larger declines with medium wools already near historic lows with the Eastern Market Indicator (EMI) expected to remain below 1,350 cents. Tasmania contributes just over two per cent to the national wool clip. Strong seasonal conditions through the first half of the year has seen an over 50 per cent increase year on year in wool volume from the state during 22/23. Decent rainfall has driven strong pasture growth which with lower sheep meat prices driving retention of ewes.

South Australia forecast

- Strong fruit and vegetable production is forecast in South Australia during the back half of the year amidst favourable weather and improving labour availability.

- This year’s almond crop has been impacted by a number of challenges, with initial estimates putting total output for the 2023 crop well below last year’s almond crop of almost 140,000 tonnes. Difficulties with pollination driven by the varroa mite outbreak last year along with a wet finish to 2022 drove a significant decline in yields.

- Orange production volumes are expected to decline slightly with average yields and slightly smaller sizing, though overall quality is looking good.

- South Australia has had a strong start to the 2023/24 cropping season with above average soil moisture conditions during the ideal planting window. Crops have established well and now widespread rainfall during June has strengthened production outlooks.

- South Australian milk production is forecast to be marginally lower year-on-year in the 2023/24 season after severe declines in 2022/23. Seasonal conditions have been favourable for pasture growth and record opening farmgate milk prices provide for an optimistic outlook for dairy which is anticipated to ease the rate of industry exits.

- Lamb markets are expected to encounter good numbers of new season lambs in the second half of 2023. As high supply continues, markets will be looking for direction from export demand which has been a mixed bag so far this year. A drier outlook should avoid the challenges presented by the wet conditions of late 2022 which culminated in a surge of supply in recent months.

- South Australian cattle prices are expected to see a continued marginal decline during the second half of 2023 due to pressure from increased supply.

- Australian wool prices will continue to come under pressure as demand eases which has driven the Southern Market Indicator to below 1,101 c/kg. The Eastern Market Indicator is expected to remain below 1,350 cents over the back half of the year.

- Current wool production in South Australia is 4.3 per cent above last season. Pastoral regions have had good rain. Merino wool producers in these regions are increasing sheep numbers with lower sheep slaughter rates which will drive strong production over the next six months.

Western Australia forecast

- Above average fruit and vegetable production is forecast across Western Australia, though dry conditions may begin to impact crops coming into summer with deep soil moisture levels currently well below those of the east coast.

- Another strong year of Hass avocado production is expected in WA as younger plantations continue to mature (just over two thirds of WA plantations are at full production age). Current estimates for 23/24 WA avocado production are at over 9 million trays (5.5 kg) which compares to 8.5 million trats in the 2021/22 season. Recently announced export access to Thailand for WA growers will be crucial in absorbing this growing supply over the coming seasons.

- Below average rainfall in May across all Western Australian cropping regions had the season sitting on a knife edge for many. Early rainfall in June has turned this around with average yields now achievable. Western Australia will take a record carry in of wheat stocks into the new season. This will see exports remain strong right up to harvest time. This strong supply of stocks will likely limit any price increases relative to international values.

- Western Australian milk production is forecast to be lower year-on-year as the trend of declining production continues, but at a slower pace. Seasonal conditions do not look as positive as last year, and labour availability remains an issue. But competition for a smaller pool will see high farmgate price offerings of around or slightly above $9.00/Kg MS maintained through to the end of 2023.

- Lamb markets are expected to encounter good numbers of new season lambs in the second half of 2023. As high supply continues, markets will be looking for direction from export demand which has been a mixed bag so far this year. A drier outlook should avoid the challenges presented by the wet conditions of late 2022 which culminated in a surge of supply in recent months.

- The West Australian sheep industry is confronting a significant disruption with the planned phase out of live sheep exports by sea. Western Australia accounted for 99.3 per cent of Australian live sheep exports in 2022. Live sheep exports from Western Australia have already seen a significant decline in recent years, falling from over one million head in 2019 to just over than 520,000 head in 2022 largely due to a cessation of trade during the Middle Eastern summer months. This accounted for 12 per cent of the state’s sheep and lamb turn-off. A report from the recent consultation period will be provided to the Minister for Agriculture, Fisheries and Forestry by 30 September 2023 providing advice on how and when the phase out will occur.

- Western Australia’s cattle prices are likely to continue marginally declining in the next six months as rising supply levels push prices down.

- Low sheepmeat and wool margins are making wool production unfavourable for mixed farmers which will see an increase in mixed farmers moving out of sheep following spring shearing.

This may see volumes trend lower after spring shearing with the Western Market Indicator to remain below 1,400 cents. Current wool production volumes for 22/23 season are broadly in line with 21/22.

{kind=link}