New report broadly optimistic as seasonal, trade conditions improve.

Rural Bank, Media Release, 12 December 2023

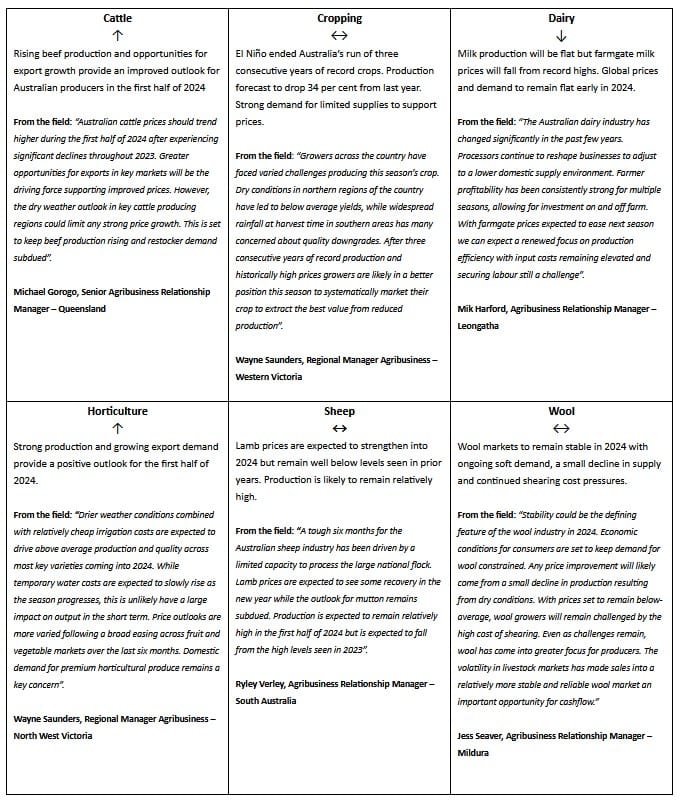

Rural Bank’s Australian Agriculture Outlook 2024 aims to help farmers make informed decisions by presenting a detailed view on how the year ahead is likely to unfold. The report finds Australian agriculture encountered a challenging environment over the back half of 2023 with drier weather leading to lower crop production but contributing to significantly higher cattle production and record lamb production as producers turned off stock in response.

Lower commodity prices also impacted Australian farmers in 2023, while improved labour supply and lower fertiliser costs provided some relief, but margins continue to remain tight. Export demand continued to rebound across the cropping and horticulture sectors, though demand for livestock and wool remained subdued, primarily due to economic pressures. Ongoing economic challenges, the prospects of a hotter summer, and below average commodity prices are weighing on the outlook for the first half of 2024.

Andrew Smith, Rural Bank Head of Agribusiness Development said: “As was the case for 2023, the three key themes that will impact Australian agriculture in the first half of 2024 continue to be seasonal conditions, trade conditions and economic headwinds, but looking to the upside, a more favourable economic environment is expected to begin supporting agricultural markets in the back half of 2024.

“Another positive is the forecast breakdown of both the El Niño and IOD climate drivers that will hopefully see a return to more average conditions for eastern Australia, benefitting the cropping sector for the winter sowing and lifting horticultural production in the first half of the year off the back of more favourable conditions for fruit and vegetable crops and lower irrigation costs.

“We expect to see growing export demand for grains and horticultural produce along with rising beef production and further opportunities for export growth in the red meat sector, improving the outlook for Australian producers in the first half of 2024. Lower lamb prices should also keep export volumes closer to current levels, but we see further appetite for lamb returning as retail prices trend lower, boosting domestic consumption, with prices likely to improve for producers in the new year”, Mr Smith said.

The report found that improving trade conditions throughout the back half of 2023 and normalisation of supply chains were a positive and will continue to support Australian agricultural exports through the first half of 2024, as will the normalisation of Australia’s trade relationship with China.

“We also see trade with India and the United Kingdom continuing to expand in 2024, with a potential trade deal with the United Arab Emirates another positive development – however, volatility in global grain markets remains a concern, driven by Russia’s ongoing invasion of Ukraine.

“Economic headwinds will again be challenging for agribusiness in the first half of 2024, with slower economic growth in major economies like the EU and US expected to affect global consumption and with farm input costs forecast to remain stubbornly above long-term averages.

“Seasonal labour costs continue to remain high with no relief in sight and elevated fertiliser and diesel prices will similarly continue to keep the cost of production high, driven by expensive gas used in fertiliser production, volatile oil production and a low Australian dollar”, Mr Smith concluded.

Fast facts are below, with the full detailed analysis available in the main report.

National commodity snapshot

Country snapshot: State by State fast facts

Queensland

- Macadamia output for the 2023 season is estimated at 48,500 tonnes in shell by the industry body. This is well down from the almost 53,000 tonnes produced last season. The lowest farmgate prices in over a decade and significant farm costs will be key factors heading into the 2024 season. We estimate production will return above 50,000 tonnes in 2024.

- Table grape production will reach near record levels this season. This strong forecast is a result of favourable conditions and low water costs. Dry weather through until harvest will ensure grapes are higher quality than last season.

- Queensland growers have finished harvesting their winter crops. Production is well down on last season with just 400 thousand tonnes of grain delivered into GrainCorp’s receival sites versus 2.1 million tonnes last season. Widespread rainfall over November will allow Queensland growers to now plant summer crops and give them a chance to offset poor returns from the 2023/24 winter crop.

- Queensland’s cattle prices are expected to continue the recent trend throughout the past month and trend marginally higher. Cattle slaughter is also expected to increase on the back of strong supply available on local markets, however with most processing centres booked out months in advance, significant growth in rates may be limited.

- Stability could be the defining feature of the wool industry in 2024. Economic conditions for consumers are set to keep demand for wool constrained. Any price improvement will likely come from a small decline in production resulting from dry conditions. With prices set to remain below-average, wool growers will remain challenged by the high cost of shearing. The Northern Regional Indicator sat at 1,214c/kg at the end of November, 9.1 per cent lower year-on-year and 17.9 per cent below the five-year average.

- Queensland milk production is expected to stabilise at around 280-285 million litres in the 2024/25 season following six seasons of declining production. Opening farmgate milk prices are expected to decline from record highs in 2023/24 where Norco is offering 88c/litre. Queensland new season farmgate milk prices may not decline as much as southern states as production is predominantly fresh milk for domestic consumption and not as strongly influenced by global pricing.

New South Wales

- Stone fruit production is expected to jump substantially this season. This follows two consecutive years of wet conditions and high input costs. The drier weather conditions and cold winter temperatures are also driving improved quality this season.

- Domestic demand for higher priced cherries may come under pressure from high cost of living pressures. Mainland states will likely see cherry prices sit slightly below average leading into Christmas due to the lower consumer demand and high production.

- Lamb markets are expected to strengthen in 2024 as the surge in supply eases. Increased processing capacity and softer retail prices are expected to see a lift in domestic consumption. The outlook is for warm and dry weather in the new year which will continue to limit restocker confidence and restrict the uplift in prices.

- It has remained a tale of two seasons for New South Wales growers. Dry conditions continued for those in northern regions with winter cereal production coming in below average. Like their Queensland counterparts, November rain will also allow for summer crop planting and hopefully offset poor results from the winter program. Growers in the south had mostly favourable growing season conditions with positive production outlooks. Rainfall over November delayed harvest and raised concerns around quality downgrades.

- New South Wales milk production is forecast to be flat to slightly higher in 2024. Those in the south had better growing season rainfall with good production outlooks. Season to date production is already 7% higher year-on-year (Jul-Sep). Dry conditions in northern areas may put the brakes on production later in the year. Processors will have to compete to secure supply but farmgate prices will ease from record highs in 2023/24.

- New South Wales cattle prices are likely to continue the recent trend from November and marginally increase throughout the first half of next year. Slaughter rates are also likely to increase with a strong supply of cattle available on local markets, however processing centre capacities could limit the potential pace at which rates rise.

- Stability could be the defining feature of the wool industry in 2024. Economic conditions for consumers are set to keep demand for wool constrained. Any price improvement will likely come from a small decline in production resulting from dry conditions. With prices set to remain below-average, wool growers will remain challenged by the high cost of shearing. The Northern Regional Indicator sat at 1,214c/kg at the end of November, 9.1 per cent lower year-on-year and 17.9 per cent below the five-year average.

Victoria

- Table grape production will reach near record levels this season. This strong forecast is a result of favourable conditions and low water costs. Dry weather through until harvest will ensure grapes are higher quality than last season, though heavy rainfall at the end of November across Sunraysia does risk a Downy Mildew outbreak. Wine grape prices are expected to see a more mixed outlook in 2024. Substantial red wine inventory levels will continue to see uncontracted red grapes remain unsold.

- Australian almond production has been forecast to rebound in 2024. Total output is estimated to rise 28 per cent to 140,000 tonnes in 2024. A varroa mite related shortage of beehives in key regions and challenging conditions were the key factors in last season’s reduced yields. Strong export demand combined with low domestic carryover stocks will also push almond prices higher over the first half of the year, though coming off a low base.

- Victorian milk production is expected to remain flat to slightly lower than 2023. Industry exits are expected to ease following a period of high profitability. Average profitability of Victorian dairy farms was the second highest in 17 years, aided by record farmgate milk prices. Weaker global dairy prices will see new season opening farmgate prices likely drop below $8.50/Kg MS as processors continue to ‘right size’ their businesses to a lower supply environment.

- Victoria was looking to be the standout state in terms of production and quality for winter crops. Early harvest results show that wheat and barley yields will exceed expectation. Widespread rainfall at the end of November halted harvest with concerns arising that a significant volume would be downgraded to feed. At the time of print, growers were cautiously optimistic that they would still have milling wheat and malting barley if December remained dry and they got a clear run at finishing harvest.

- Lamb markets are expected to strengthen in 2024 as the surge in supply eases. Increased processing capacity and softer retail prices are expected to see a lift in domestic consumption. The outlook is for warm and dry weather in the new year which will continue to limit restocker confidence and restrict the uplift in prices.

- Victoria’s cattle prices are likely to continue the recent strong growth recorded throughout November into the first half of 2024. Whilst strong export demand will likely apply upwards pressure on prices, it is expected that prices will remain below the five-year average. Cattle slaughter is likely to continue to increase during the next six months, however with most processing centres booked out over three months in advance this could limit the potential pace at which slaughter rates lift.

- Stability could be the defining feature of the wool industry in 2024. Economic conditions for consumers are set to keep demand for wool constrained. Any price improvement will likely come from a small decline in production resulting from dry conditions. With prices set to remain below-average, wool growers will remain challenged by the high cost of shearing. The Southern Regional Indicator sat at 1,140c/kg at the end of November, 5.2 per cent lower year-on-year and 16.9 per cent below the five-year average.

Tasmania

- Onion production volumes across Australia remains slightly above average. Relatively good yields and quality have been seen across key growing regions following dry weather. Poor EU output will ensure export demand for Tasmanian onions remains elevated for the second season. Tasmanian onion harvest should be in full swing by January. European shortages will peak around March which is well timed with the Tasmanian harvest.

- Stone fruit production is expected to jump substantially this season. The drier weather conditions and cold winter temperatures are also driving improved quality this season. As a result, the USDA are estimating cherry output will increase by 18 per cent. Exports are also forecast to lift substantially from last season. This surge in exports is the result of the strong output, higher quality and resurgent demand from China.

- Tasmanian milk production has performed well relative to other states. Season to date production is up 2.3 per cent year-on-year but is still 3.6 per cent below average. 2023/24 production is estimated to finish above last season’s 916 million litres but will likely finish below the five-year average of 925 million litres. Farmgate prices are expected to ease from record highs in the 2022/23 season as softer global prices will see processors reduce opening bids.

- Lamb markets are expected to strengthen in 2024 as the surge in supply eases. Increased processing capacity and softer retail prices are expected to see a lift in domestic consumption. The outlook is for warm and dry weather in the new year which will continue to limit restocker confidence and restrict the uplift in prices.

- Tasmania’s cattle prices are likely to continue to rise throughout the first half of 2024, capitalising on the strong growth during November. Strength in export demand is expected to provide a marginal boost to cattle prices, however the dry weather outlook may apply downwards pressure on prices.

- Stability could be the defining feature of the wool industry in 2024. Economic conditions for consumers are set to keep demand for wool constrained. Any price improvement will likely come from a small decline in production resulting from dry conditions. With prices set to remain below-average, wool growers will remain challenged by the high cost of shearing. The Southern Regional Indicator sat at 1,140c/kg at the end of November, 5.2 per cent lower year-on-year and 16.9 per cent below the five-year average.

South Australia

- Australian almond production has been forecast to rebound in 2024. Total output is estimated to rise 28 per cent to 140,000 tonnes in 2024. A varroa mite related shortage of beehives in key regions and challenging conditions were the key factors in last season’s reduced yields. strong export demand combined with low domestic carryover stocks will also push almond prices higher over the first half of the year. Though coming off a low base.

- Wine grape prices are expected to see a more mixed outlook in 2024. Substantial red wine inventory levels will continue to see uncontracted red grapes remain unsold. We don’t anticipate further reductions in red wine grape prices. Though they are unlikely to lift from current lows for the 2024 vintage. White grape producers remain in a better position, with a more sustainable supply and demand outlook.

- South Australia had a strong start to the 2023/24 cropping season with average to above average rain up to the end of June. In the subsequent months totals fell below average along with the state’s production outlook. Total winter crop production is forecast at 8.2 million tonnes, a 33 per cent decline from last season’s record production.

- South Australian milk production is expected to lift marginally after 2022/23 supply hit a five-year low. While not as good as previous seasons, pasture growth has been favourable with late spring rains, though quality is compromised. Anticipated lower farmgate prices will squeeze margins for producers as input costs remain elevated.

- Lamb markets are expected to strengthen in 2024 as the surge in supply eases. Increased processing capacity and softer retail prices are expected to see a lift in domestic consumption. The outlook is for warm and dry weather in the new year which will continue to limit restocker confidence and restrict the uplift in prices.

- South Australia’s cattle prices are forecast to increase throughout the next six months, as strong export demand continues to provide support for local prices.

- Stability could be the defining feature of the wool industry in 2024. Economic conditions for consumers are set to keep demand for wool constrained. Any price improvement will likely come from a small decline in production resulting from dry conditions. With prices set to remain below-average, wool growers will remain challenged by the high cost of shearing. The Southern Regional Indicator sat at 1,140c/kg at the end of November, 5.2 per cent lower year-on-year and 16.9 per cent below the five-year average.

Western Australia

- Western Australian fruit and vegetable production is forecast to remain in line with average, though dry conditions are beginning to impact grower sentiment.

- A dry finish to the season for Western Australian growers has led to a significant drop in production from last year. The state’s main grain handler CBH is expecting to receive 13.5 million tonnes into their sites compared to last seasons record 22.4 million tonnes. The dry finish has seen higher protein levels in wheat compared to the last couple of seasons. Strong export demand from the reopened Chinese market has kept feed barley prices at impressive levels and has been a strong sell for growers over harvest.

- Margins for milk producers will come under pressure in 2024. Labour availability remains a challenge and wage pressures add to reduced fodder production in drier regions and elevated input costs. Farmgate prices are forecast to ease and lower cattle prices add to margin stress. Despite this, milk production is expected to lift slightly in 2023/24, with season to date production up 4 per cent year-on-year, and just 0.6 per cent below average.

- Lamb markets are expected to strengthen in 2024 as the surge in supply eases. Increased processing capacity and softer retail prices are expected to see a lift in domestic consumption. The outlook is for warm and dry weather in the new year which will continue to limit restocker confidence and restrict the uplift in prices. The Western Australian sheep industry will continue to wait on the outcome of the independent panel’s report into the phase out of live sheep exports. How the government plans to implement the phase out will have a large bearing on grower confidence in 2024.

- Western Australian cattle prices are expected to continue marginally increasing during the next six months as strong export demand pushes prices up.

- Stability could be the defining feature of the wool industry in 2024. Economic conditions for consumers are set to keep demand for wool constrained. Any price improvement will likely come from a small decline in production resulting from dry conditions. With prices set to remain below-average, wool growers will remain challenged by the high cost of shearing. The Western Regional Indicator sat at 1,316c/kg at the end of November, 6.5 per cent lower year-on-year and 12.5 per cent below the five-year average.

To view the full Rural Bank Australian 2024 Outlook report, visit: https://www.ruralbank.com.au/knowledge-and-insights/.

{kind=link}