Rabobank, Media Release, 9 March 2023

According to a new report from Rabobank, participants all along the dairy value chain are being squeezed. Producers’ milk prices have tumbled from 2022’s lofty levels while feed prices are at record highs. Processors and dairy cooperatives entered the year discounting expensive inventory made with high-priced milk. Meanwhile, higher inflation and rising interest rates are pressuring consumers toward more frugal purchasing behaviour.

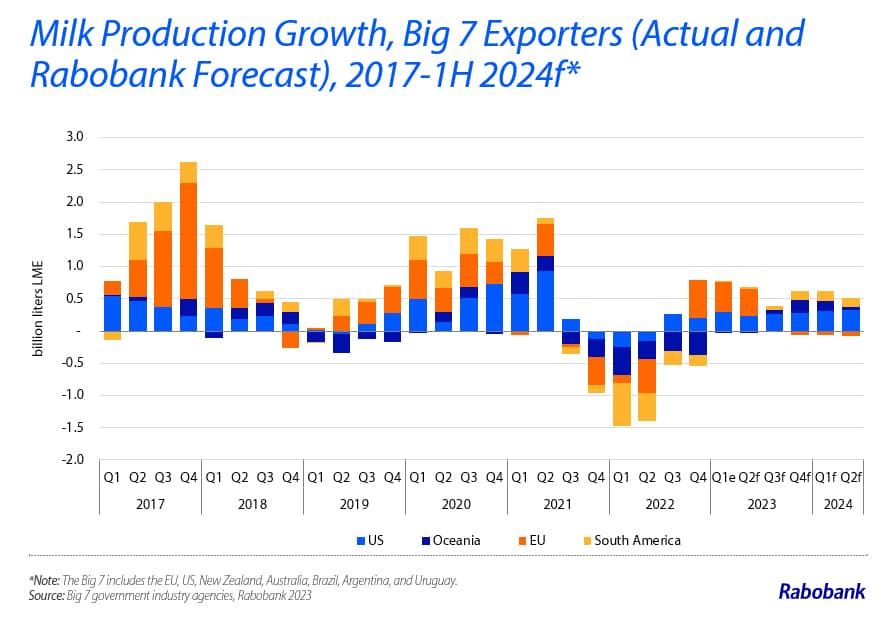

Greater year-on-year milk production growth has emerged in 2023 in the key export regions, compared to 2022’s low levels. At the same time, farmgate milk prices are catching up to global commodity market trends and have moved lower. Expensive input costs remain a clear headwind worldwide and, combined with lower milk prices, are resulting in farm-level margin pressure. In response, dairy cow slaughter rates have escalated.

“Milk production from the Big 7 export regions is anticipated to grow by 0.7% year-on-year in 2023, following 2022’s decline of 0.9%,” says Mary Ledman, Global Sector Strategist for Dairy at Rabobank. “Rabobank downgraded its 2023 forecast from last quarter’s estimate of 1%. This slower growth is attributed to increased culling in the US and weather-related production challenges in New Zealand, Brazil, and Argentina.”

Price uncertainty continues

Dairy market price uncertainty remains across regions and dairy products. A little more milk and a little less demand have contributed to weaker dairy commodity prices in Q1 2023. However, stock levels in the key exporting regions are not burdensome. Cheese and butter prices have performed the best, while skim and whole milk powder markets have yet to find sound footing.

Consumers are part of the story. In a complex macroeconomic environment, with core services inflation remaining strong, there are increased signs of a slowdown in household consumption, which is likely to continue deteriorating over the coming months. “Consumers haven’t left the dairy aisle,” says Ledman, “but they are looking for value.”

Eyes on Chinese demand

Lower global cheese, milk powder, and whey prices, year-on-year, are expected to support exports. Still, much depends on internal Chinese policies and broader demand resilience to support dairy product prices in 2023.

Global dairy trade in 2022 was better than expected, despite China’s retreat. Exports to key importers including Mexico, Indonesia, Japan, Algeria, and South Korea, among others, surpassed 2021 levels. “Through November 2022, trade in total dairy product volume was within 1.5% of the previous year, despite about a 20% reduction in China’s imports,” notes Ledman. With China’s reopening, Rabobank forecasts foodservice revenues there to improve by 1% to 2% compared to pre-Covid levels. “Looking ahead, China’s dairy imports in the first quarter of 2023 are expected to fall short of year-ago levels, with renewed buying interest developing in the second quarter of the year. We expect a mild year-on-year increase in imports in the second half of 2023.”

{kind=link}