Rabobank Wine Quarterly Q2 2022

Rabobank, Media Release, 6 April 2022

Stephen Rannekleiv.

The global wine sector is facing significant disruptions in different links of the supply chain. The common assumption was that these issues were transitory. Now there are increasing signs that some of these changes are structural and could even get worse, requiring more strategic responses.

Since the middle of 2021, at least five aspects of the global wine supply chain – including agricultural production, freight, labor, geopolitics, and energy – started to face significant disruption all at once, causing wineries around the world headaches.

“Some of these disruptions have been driven by short-term cyclical factors and may see improvements in the near to medium term. Unfortunately, others are starting to appear to be more structural in nature,” says Stephen Rannekleiv, Global Strategist – Beverages at Rabobank. The global wine industry in its current state has evolved in a context of cheap freight, cheap energy, and declining trade barriers.

Many challenges facing the wine industry, with uneven impact

The five key factors that are challenging the sector can be listed as:

- Freight: Shipping rates for containers experienced exponential increases in 2021. This rise in freight costs – of 200% or more in some cases – and sporadic shipping availability, have led to a dramatic increase in the cost of importing wine in some markets.

- Fuel: Brent Crude oil prices have risen 70% since March 2021. Natural gas prices in Europe have risen 550% over the same period. These rising fuel costs are hitting producers around the world, and are felt all along the supply chain

– from fertilizer costs, operating costs, transportation, and packaging. The vast majority of wine is sold in glass bottles, which is an energy-intensive operation. Packaging costs – of which glass is the largest component – can account for 12% to 35% of a winery’s cost of goods sold. - Labor: The impact of rising labor costs is not just felt in the vineyard, but also in wine production, transportation and sales, with a bigger impact in some regions than others.

- Geopolitics: The direct impact of numerous geopolitical developments in recent years has caused volatility and disruptions in the global industry.

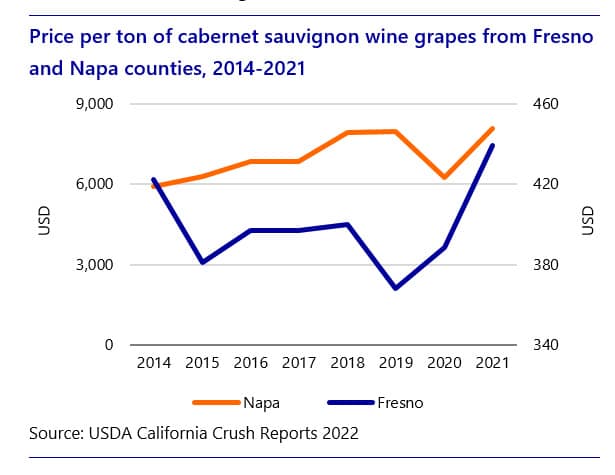

- Ag Production: In 2021 Europe had one of the lightest grape harvests in decades. In the US – the largest wine producer outside of Europe – the 2021 wine grape crop was below average. As a result, inventories are relatively tight, keeping upward pressure on bulk wine pricing in most regions.

The impact of this variety of disruptions is felt very differently by wineries in different regions or price segments. Wineries in Europe have been hit to a much larger degree than other regions. European producers are taking the greatest brunt of rising energy costs. For producers in Australia, geopolitical factors have had the greatest impact by far. In 2021, exports to China, their largest market, fell by 97%, after China imposed tariffs of 166% to 218% on imports of Australian wine.

Strategic solutions are needed

“As wineries grapple with so many disruptions, the immediate responses have been more tactical than strategic. This makes sense because it has not always been clear which challenges were short-term cyclical issues, and which changes were likely more structural in nature,” says Rannekleiv. However, we would argue that energy prices and geopolitical factors are more structural in nature, and any ‘solutions’ moving forward should take them into account.

“We need to reassess supply chains with a fresh, creative perspective. Old assumptions that have formed the basis of the current operating model, like free trade, cheap fuel, and cheap freight, should be questioned. It is important to rethink how to thrive in a context where the rules of the game are different,” according to Rannekleiv.

Pricing actions have been wineries’ first and most obvious line of defense to try to maintain margins. But as consumers face rising cost pressures for numerous basic staples, other more structural and strategic responses may be worth considering. These could include complete rethinking of packaging; shifting more of the supply chain operations closer to the end consumer where possible to improve efficiency; and diversifying – of markets and/or sourcing – to help mitigate geopolitical risks.

{kind=link}