Over the weekend Michael Cannon-Brookes, co-founder of listed software company Atlassian Corporation plc (NASDAQ:TEAM), announced that he had lodged a takeover offer, in conjunction with Canadian infrastructure giant Brookfield Asset Management (NYSE:BAM), for the listed Australian energy giant, AGL (ASX:AGL). Cannon-Brookes is making the offer through Grok Ventures, the private investment company owned by himself and his wife Annie Cannon-Brookes.

Commenting on the proposal, Cannon-Brookes stated:

“This proposal will mean cheaper, cleaner and more reliable energy for customers. It will create over 10,000 Australian jobs and ensure customers don’t bear the brunt of higher power

prices – a likely scenario if the proposed demerger happens.

“AGL accounts for over 8% of Australia’s emissions: – more than the current emissions of Australian domestic and international aviation combined, or every car on the road in Australia. As a country, it emits more than Sweden, Ireland or New Zealand. If successful, this will be one of the biggest decarbonisation projects in the world today and show Australia is capable of globally significant projects.”

Given the importance of AGL’s assets in the eastern seaboard energy network and the stated intention of Cannon-Brookes and Brookfield to bring AGL’s current net zero target forward by 12 years to 2035, principally by closing some of AGL’s coal-fired power stations early, Kookaburra decided to take a closer look at Cannon-Brookes and the company with which he is most associated, Atlassian.

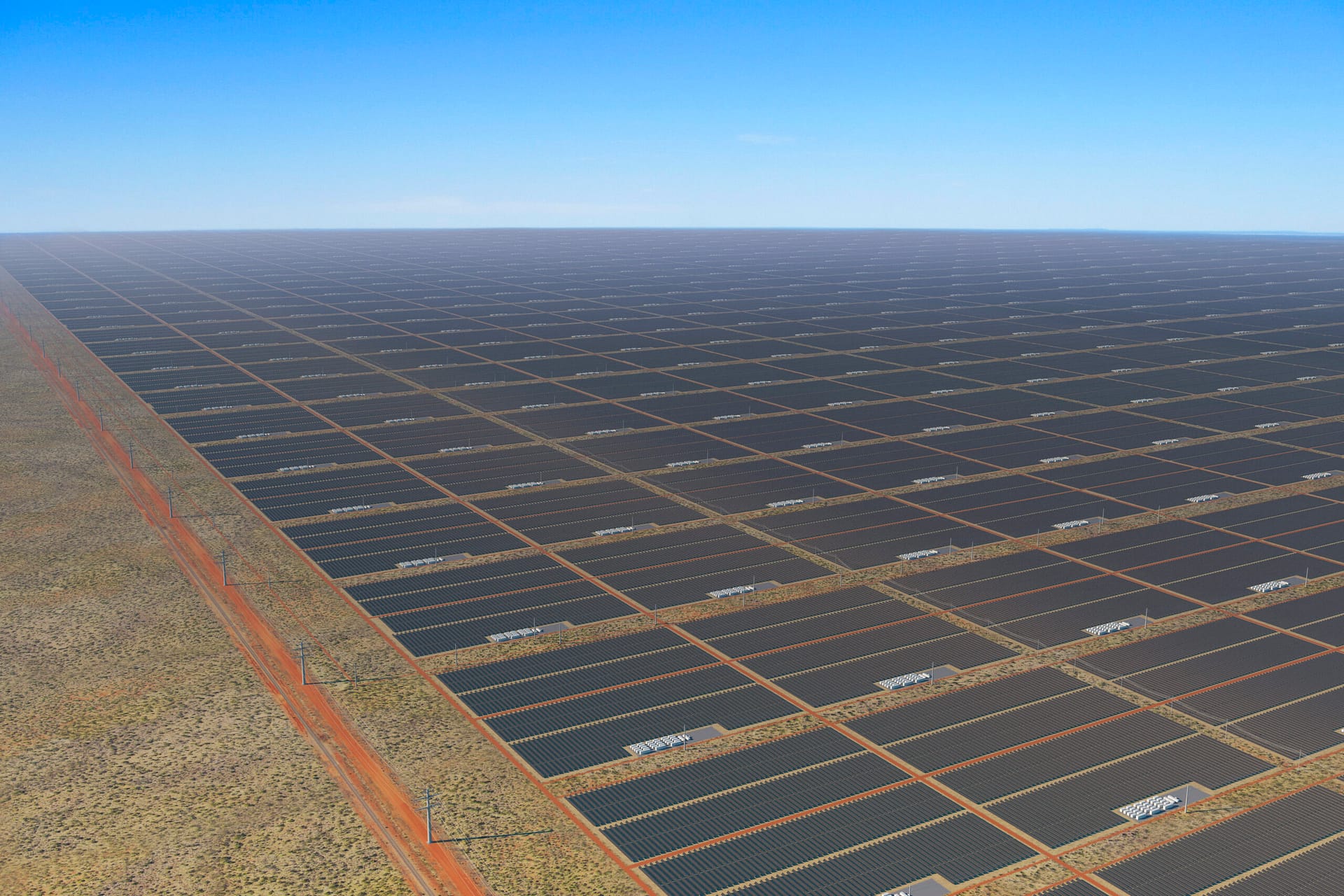

This is not the first time Cannon-Brookes has shown interest in being involved in the energy industry. He has partnered with Andrew Forrest in developing the solar power explorer, Sun Cable, whose prime asset is its solar farm near Tennant Creek in the Northern Territory.

Sun Cable is building one of the world’s largest renewable energy infrastructure projects, the AUD30+ billion Australia-Asia PowerLink (AAPowerLink), which is intended to supply renewable electricity to Darwin and Singapore.

Sun Cable concluded a significant capital raising in November 2019, with cornerstone investment from Mike Cannon-Brookes’s Grok Ventures and Andrew Forrest’s Squadron Energy, together with a range of private investors.

However, this project suffered a blow when iSwitch Energy, a Singapore-based independent electricity retailer, which had earlier, in March 2021, pledged to be a buyer of the solar energy from Sun Cable, announced, in October 2021, that it would exit the retail electricity market due to soaring energy prices in Asia.

The company to which iSwitch is switching its retail customers, SP Group, announced, on 12 October 2021, that it and France’s energy developer Electricite de France (EDF Group) (EDF:FP) had signed a memorandum of understanding (MOU) on 11 October 2021 and had agreed to partner on a renewable energy supply project supplying energy from Indonesia to Singapore.

Sun Cable is just one of a number of ‘green’ projects and companies in which Cannon-Brookes has invested.

The Australian Financial Review reported that the Prime Minister, Scott Morrison, revealed that Brookfield owns 80 per cent of the consortium which would suggest that Cannon-Brookes’s investment in just the acquisition alone of AGL would be around $1 billion.

Cannon-Brookes appears to be extremely successful. The media in Australia regularly praise the success of Atlassian, the company which Cannon-Brookes and his business partner, Scott Farquhar, commenced 21 years ago in 2001, using a credit card for funding. Atlassian Corporation Plc, through its subsidiaries, designs, develops, licenses, and maintains various software products worldwide.

Whilst many people assume that Atlassian is an Australian company, it is incorporated in the United Kingdom.

On 10 December 2015, Atlassian made its initial public offering (IPO) on the NASDAQ stock exchange in New York, under the symbol TEAM. Atlassian’s market capitalisation based on its current stock price of $US290 is around $US75 billion.

According to a recent Schedule 13G filing dated 31 December 2021 filed with the United States Securities and Exchange Commission, Cannon-Brookes and CBC Co Pty Ltd as trustee of the Cannon-Brookes Head Trust hold a combined total of 55,816,134 Class B shares in Atlassian. According to a similar filing, Scott Farquhar and Skip Enterprises Pty Limited as trustee of the Farquhar Family Trust hold also hold 55,816,134 Class B shares in Atlassian. Based on the stock price of $US290, this would place a value of $US16,186,678,860 on Cannon-Brookes’s shareholding – so, around $US16.1 billion.

What is so special about Class B shares as opposed to the Class A shares which are traded on the exchange? This is explained in Note 3 in the filings ‘Each Class A ordinary share is entitled to one vote and each Class B ordinary share is entitled to ten votes’. In other words, holders of Class B shares have ten times the voting power of holders of Class A shares.

$US16.1 billion is a large sum. However, until a purchaser pays a seller, it is somewhat theoretical. Yet would this wealth be enough to support what Cannon-Brookes apparently wishes to achieve? Is Atlassian itself profitable?

Atlassian’s profitability

In its early years, Atlassian had good cash flow and made profits. However, since going public in December 2015, Atlassian has shown a net positive income result in only four of the last 24 quarters (the last 6 years).

As the company has grown, so have the challenges. Growth has been achieved largely through acquisition, costly within itself, and uncertain in terms of outcomes. In order to remain competitive, Atlassian has had to invest heavily in research and development – approximately $US3.7 billion since 2014.

Despite these investments in acquisitions and research and development, growth in subscriber numbers slowed by approximately 13% in the quarter ending 31 December 2021. Profitability remains elusive. The rates of growth in costs of revenues and total operating expenses are outpacing the rates of growth in total revenues, gross profit and net income.

Far from its early days of showing retained earnings – hitting a high of $US23,977,000 in the March quarter of 2016 – Atlassian now shows an accumulated deficit of $US2,290,281,000 as at 31 December 2021.

Atlassian does not pay dividends. This may not be such a concern with an ever-increasing share price, but even that star has ceased to shine as brightly as it did, with the share price, once seen heading to $US500, now hovering around the $US290 mark.

According to filings with the United States Securities and Exchange Commission, between December 31, 2015 and December 31, 2021 both Cannon-Brookes and Farquhar have each reduced their holdings in Atlassian from 69,732,090 shares to 55,816,134. A reduction of 13,915,956 shares or approximately 20% of their initial holdings.

The average stock price between the open and today was $US127.35 with many gyrations up and down between the low of $US20.77 on 29 January, 2016 and the high of $US458.13 on October 29, 2021.

Exchangeable Senior Notes

Given these dynamics, Atlassian has necessarily turned to borrowings of one form or another. One of those borrowings was for $US1 billion by way of what were described in Atlassian’s announcement on 30 April 2018 as Exchangeable Senior Notes.

The Quarterly report (Form 6-K) issued on 26 July 2018, referred to the Exchangeable Senior Notes.

The Exchangeable Senior Notes could be redeemed only for cash (not stock) and their value at the time of redemption was to be calculated based on a formula which included reference to the stock price. So, it appeared that the arrangement meant that, as the share price increased, so would the return to the holders of the Notes. Being an off-market transaction, it was not necessary for Atlassian to notify the market as to the identity of the Note holders.

The next we hear of the Notes is in two filings by Atlassian in which reference is made to the repayment of the Notes. The first, on Page F-9 of the Atlassian Annual Report dated 30 June 2021, stated that during fiscal year 2021 an amount of approximately $US1,803,244,000 had been paid to the Note holders. The second, on Page 8 of the Earnings Release, dated 27 January 2022, stated that an amount of approximately $US1,548,686,000 had been paid to the Note holders.

So, for their initial $US1 billion investment, it would appear that the un-named Note holders have received approximately $US3,351,930,000 – about $US3.3 billion. Not a bad return on investment in around three years. Especially when the company providing this return, even after over 20 years of existence, makes no regular profits, pays no dividends, has a depreciating share price and has an accumulated deficit of approximately $US2.2 billion.

At the time of writing, the board of AGL had rejected the approach of Cannon-Brookes and Brookfield.

The announcement of the offer for AGL made by Brookfield Asset Management and Grok Ventures can be found here.

Atlassian Investor Relations can be found here: https://investors.atlassian.com/ir-home/default.aspx

In response to a request for comment on this story by Australian Rural & Regional News, Atlassian provided the comment from Cannon-Brookes on the proposal made to AGL included above and further information about the proposal.

{kind=link}