Signs of weakening demand for dairy are spreading across markets

Rabobank, Media Release, 15 June 2023

According to a new report from Rabobank, the cumulative effects of high food price inflation over the past 24 months, along with slowing economic activity in 2023, have translated into lower dairy demand in developed and emerging markets.

Various companies in western Europe, Australia, Brazil, China, and other emerging markets are experiencing weaker-than-expected sales in 2023 (mostly in volume terms). Households in many regions remain under financial pressure, which is impacting food purchasing behavior. One notable exception is the US, where current consumer demand for dairy products remains firm. “Some price deflation in dairy could help sustain demand levels in key markets during the second half of 2023,” notes Andrés Padilla, Senior Analyst – Dairy at Rabobank.

Production growth losing momentum

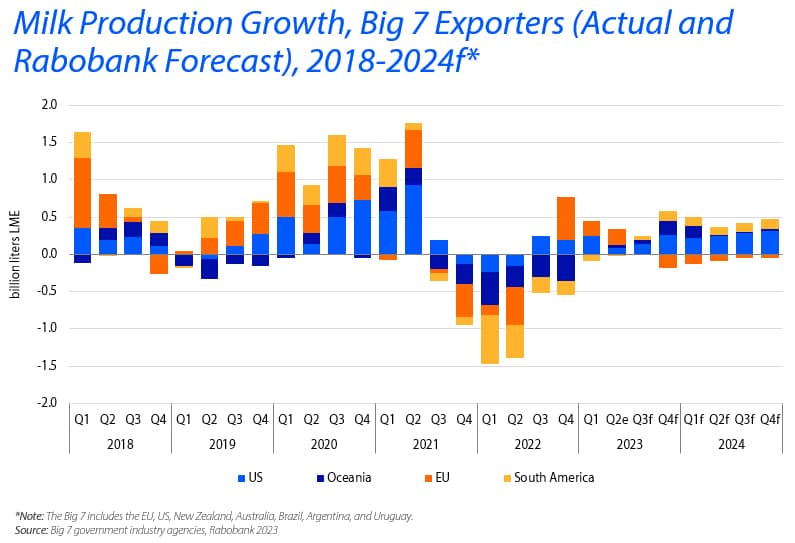

Global milk production is still rising but losing momentum, and that slower production increase could stabilize global market prices. Growth is attributed to EU and US gains, while Oceania and South America continue to see lower output in 1H 2023. Dry weather in South America and parts of Europe must be monitored and could be a key factor impacting production during Q3, particularly in Europe. “Our current outlook for lower production in the EU and US, with limited growth elsewhere, is likely to support global dairy prices in Q3 and into 2024,” states Padilla.

Australia

For Australia, the rate of decline in milk production continued to moderate in April, with national milk production down 1.7 per cent year-on-year. This brings season-to-date milk production to 6.9 billion liters, which represents a fall of 5.9 per cent versus last season. Rabobank senior dairy analyst Michael Harvey said there were “green shoots” in some regions, with milk production growing again in March in NSW, Tasmania and Western Australia. Rabobank expects Australia’s milk production to close the season down five per cent.

Mr Harvey said the sharp fall in milk production continues to take a toll on export volumes. Season-to-date total export volumes are down 14 per cent. There are widespread declines across the product mix. On a tonnage level, the most significant decreases have been in ingredients, particularly skim milk powder (SMP) and butter. Liquid milk volumes are also under pressure, as high farmgate prices reduce competitiveness in key export markets.

Rabobank is forecasting minimum price offers for new season milk in southern Australia to be between AUD 8.50/kgMS and AUD 9.00/kgMS.

The June 1 deadline has provided the latest minimum price offers for 2023/24 milk prices. Rabobank’s Mr Harvey said across the southern Australian region, prices are broadly in line with the bank’s expectation, with a formal bandwidth of AUD 8.60 to AUD 9.10/kgMS. While generally lower than 2022/23 full-year prices, these signals ensure another season of historically elevated milk prices that will support farmgate margins.

More affordable feed brings farmers relief

Lower input costs are providing some relief to farm-level margins. Continued optimism about Brazil’s second corn crop, combined with large Russian grain exports, renewal of the Black Sea Grain Initiative, a good upcoming EU harvest, and accelerated US corn planting, continue to drive prices lower. More affordable feed provides dairy farmers some relief as farmgate milk prices decline globally. However, Chinese dairy farm margins remain under pressure despite falling feed prices. And in the US, lower milk prices have outpaced the decline in feed costs, putting farmers’ margins under additional pressure and into negative territory – a sharp contrast to the close-to-record profitability farmers experienced this time last year.

Weak Chinese demand pressures prices

To date, China’s dairy demand recovery has not offset strong domestic milk production growth. Farm expansions and continued gains in milk yields are driving domestic milk production higher, and supply may take longer than previously forecast to respond to weakening milk prices and comparatively higher feed costs. Meanwhile, Chinese dairy imports (liquid milk equivalent, excluding whey) declined in Q1 2023, adding pressure to already weaker global prices in the short term. With no immediate signal of a swift recovery in consumer demand, Chinese traders may remain cautious about returning to the market, or such a return may largely be motivated by competitive international prices and efforts to build reserves.

{kind=link}